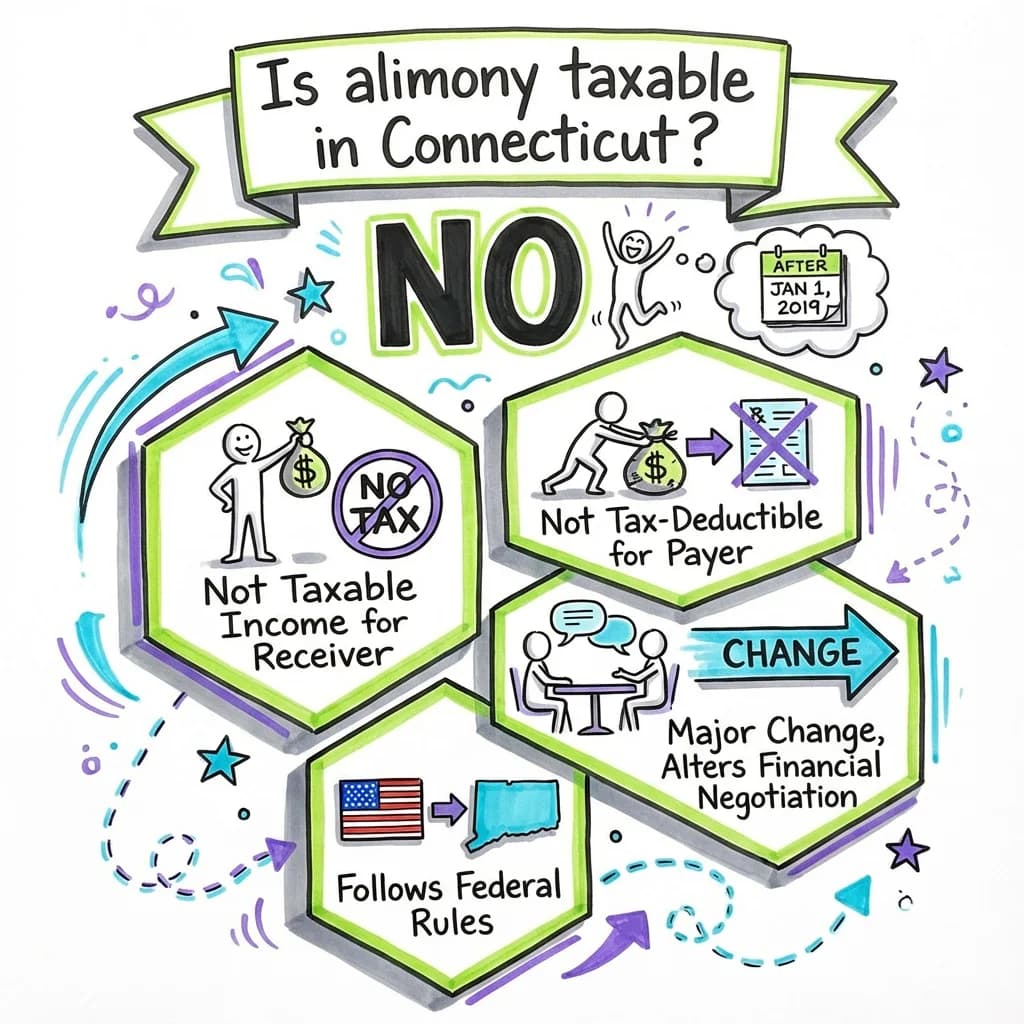

Is alimony taxable in Connecticut?

The short answer is no. For any divorce finalized on or after January 1, 2019, alimony is no longer taxable income for the person receiving it, nor is...

Need help with your divorce? We can help you untangle everything.

Get Started Today

The short answer is no. For any divorce finalized on or after January 1, 2019, alimony is no longer taxable income for the person receiving it, nor is it tax-deductible for the person paying it. This applies at both the federal and state levels, as Connecticut's tax laws follow the federal rules on this issue.

This was a major change from the old system, and it has significantly altered how finances are negotiated during a Connecticut divorce. If your divorce or separation agreement was finalized before 2019, the old rules likely still apply, meaning the recipient pays taxes on the alimony they receive. Understanding which set of rules applies to you is absolutely critical for your financial stability both during and after the divorce process.

Navigating the financial complexities of divorce can be incredibly stressful. You're not just untangling a life together; you're making decisions that will impact your financial future for years to come. This guide will walk you through everything you need to know about whether alimony is taxable in Connecticut, helping you understand the law, its practical impact, and how to protect yourself.

Understanding the Big Change: The Tax Cuts and Jobs Act (TCJA)

For decades, the tax treatment of alimony was consistent. The person paying alimony could deduct the payments from their income, and the person receiving it had to claim it as taxable income. The logic was that this shifted income from a higher tax bracket (the payer) to a lower one (the recipient), leaving more money within the family unit as a whole after taxes.

The federal Tax Cuts and Jobs Act (TCJA) of 2017 completely upended this system.

- For Divorce Agreements Finalized Before January 1, 2019 (The "Old Rules"): Alimony is tax-deductible for the payer and taxable income for the recipient. This rule continues to apply to these older agreements.

- For Divorce Agreements Finalized On or After January 1, 2019 (The "New Rules"): Alimony is paid with post-tax dollars. The payer gets no deduction, and the recipient receives the money tax-free.

Because Connecticut income tax law conforms to these federal changes, the rules for whether alimony is taxable in Connecticut are the same. This shift has a massive ripple effect on how alimony is calculated and negotiated in every divorce case.

Connecticut Alimony Law: The Foundation

While federal law dictates the tax treatment, the decision to award alimony in the first place is purely a matter of Connecticut state law. In Connecticut, alimony is financial support that one spouse may be ordered to pay to the other during or after a divorce. Its purpose is to help the lower-earning spouse maintain a standard of living and become self-sufficient.

The Superior Court has the authority to order alimony at the time it enters a divorce decree. According to Connecticut General Statutes (C.G.S.) § 46b-82(a), when deciding whether to award alimony and for how long, the court must consider a wide range of factors. These include:

"...the length of the marriage, the causes for the... dissolution of the marriage or legal separation, the age, health, station, occupation, amount and sources of income, earning capacity, vocational skills, education, employability, estate and needs of each of the parties and the award, if any, which the court may make pursuant to section 46b-81..."

The court also considers whether one parent has custody of minor children and if that affects their ability to work. It's a comprehensive look at your entire financial picture, not a simple formula.

The Real-World Impact of Non-Taxable Alimony on Your Divorce

The change in tax law fundamentally alters the value of every dollar of alimony. Both parties need to understand what this means for their bottom line during negotiations.

For the Paying Spouse

Under the new rules, you are paying alimony with money you have already paid taxes on. This makes the real cost of alimony significantly higher for you. For example, if you are in a 30% combined tax bracket, paying $1,000 in alimony under the old rules only "cost" you $700, because you could deduct the payment. Now, that same $1,000 payment costs you the full $1,000. This is a critical factor when budgeting and making settlement offers.

For the Receiving Spouse

The money you receive is yours to keep, free from federal and state income tax. This provides certainty and simplifies budgeting. However, because the paying spouse no longer gets a tax deduction, they will likely offer a lower gross alimony amount during negotiations. A $3,000 per month tax-free payment today might be equivalent to a $4,000 per month taxable payment under the old rules. It's essential to analyze any offer based on its after-tax value.

How It Changes Negotiations

The focus of alimony negotiations has shifted from a pre-tax number to a post-tax one. This requires a different mindset. Instead of arguing over a gross amount and letting the tax consequences fall where they may, you are now directly negotiating the net transfer of wealth between you.

This is why the financial statement is the most important document in your divorce. Required by the Connecticut Practice Book § 25-30, this sworn document details your income, expenses, assets, and debts. It provides the court and your spouse with a clear picture of your financial reality, which is the foundation for any discussion about the Connecticut alimony tax rules and the final award.

Alimony vs. Child Support vs. Property Division: Why Labels Matter

It's easy to get these terms confused, but their tax treatments are very different, and using the wrong label in your divorce decree can have serious consequences.

- Child Support: Child support has always been non-deductible for the payer and non-taxable for the recipient. The TCJA did not change this. The state uses the Connecticut Child Support Guidelines to calculate the amount, which is based on the parents' combined net income. The parents' obligation to support their children is outlined in C.G.S. § 46b-84.

- Property Division: When you divide marital assets like the house, retirement accounts, or investments, it is generally not a taxable event at the time of the divorce. Under C.G.S. § 46b-81, the court can "assign to either spouse all or any part of the estate of the other spouse." You don't pay taxes on receiving the house, but you may have to pay capital gains tax later if you sell it.

- Alimony: This is the only category of payment that had its tax treatment changed by the TCJA.

Clearly defining each payment in your final settlement agreement is crucial. If you agree that one spouse will pay the other $2,000 per month for five years as part of the property settlement, but you mistakenly label it "alimony" in the decree, the IRS could create problems down the road. Your agreement must be precise to ensure the tax implications align with your intentions.

Modifying an "Old" Divorce Agreement (Pre-2019)

What if you were divorced in 2017 and are still paying or receiving alimony? The old rules (payer deducts, recipient pays tax) still apply to your original agreement.

However, if you go back to court to modify the alimony amount, you have an important choice. According to the TCJA, you and your ex-spouse can explicitly agree in writing as part of the modification order to adopt the new, non-taxable rules.

This is a major financial decision and should not be made lightly. Switching to the new system will reduce the payer's "real" cost and increase the recipient's "real" gain. This change in tax treatment should be a key point of negotiation when discussing a new alimony amount. Without a clear, written provision in the modification order, the IRS will assume the original tax treatment continues.

Frequently Asked Questions About Taxable Alimony in Connecticut

Here are answers to some common questions people have about the Connecticut alimony tax rules.

1. My divorce was finalized in 2017. Is the alimony I receive still taxable in Connecticut?

Yes. Any divorce decree finalized before January 1, 2019, falls under the old rules. The person paying the alimony can deduct it on their tax returns, and you, as the recipient, must report it as taxable income. This will not change unless you and your ex-spouse go back to court and formally modify your agreement to adopt the new tax rules.

2. For my new divorce, can my spouse and I agree to make the alimony taxable like it used to be?

No. For divorces finalized in 2019 or later, the federal law is clear: alimony is not deductible by the payer or taxable to the recipient. You cannot privately agree to "opt-in" to the old system. The tax treatment is set by the date of your final divorce decree.

3. How does the court decide the amount of alimony now that it's not taxable?

The court considers the exact same factors listed in C.G.S. § 46b-82. However, judges, attorneys, and mediators are all fully aware of the new tax laws. They understand that a $1,000 payment is now a net transfer of $1,000. The final amount awarded or negotiated will reflect this post-tax reality, meaning the gross numbers may seem lower than they were in cases decided under the old rules.

4. Is lump-sum alimony taxable in Connecticut?

No. Whether alimony is paid in a single lump sum or in periodic monthly payments, the tax treatment is the same. If it is part of a divorce decree finalized after 2018, it is not considered taxable income for the recipient.

5. What if our agreement calls payments "unallocated family support" instead of alimony?

This can be very complex. "Unallocated support" (a single payment for both alimony and child support) was more common under the old tax system. Under the new rules, it's critical to be clear. Since child support and alimony have different legal end-dates and modification standards, most agreements now list them as separate payments. How the IRS would treat an "unallocated" payment depends on the specific language in your decree. Clear labeling is your best protection against future tax issues.

6. Does the non-taxable status of alimony affect my child support calculation?

Yes, it can. The Connecticut Child Support Guidelines are based on each parent's net income after taxes. Since alimony you receive is no longer part of your gross taxable income, it can change the net income figure used in the child support worksheet. This interplay between alimony and child support is a key reason why it's so important to work with a professional who can run different scenarios for you.

7. Where in my divorce paperwork will the alimony terms be specified?

The alimony amount, duration, and terms will be detailed in your Separation Agreement. This is the comprehensive legal contract that you and your spouse negotiate. Once the court finds the agreement to be "fair and equitable" under C.G.S. § 46b-66, it is incorporated by reference into your final divorce decree and becomes an enforceable court order.

Getting Help: Navigating Alimony and Taxes in Your Divorce

The question "Is alimony taxable in Connecticut?" seems simple, but the answer has complex financial consequences. The shift in tax law has made it more important than ever to have a clear understanding of your financial situation and the long-term impact of any settlement.

- Consult a Connecticut Divorce Attorney: An experienced family lawyer can explain how these rules apply to your specific situation, help you negotiate a fair agreement, and ensure your final decree is drafted correctly to protect you from future tax problems.

- Work with a Financial Advisor or CPA: A financial professional can model different settlement scenarios, helping you understand the true after-tax value of any proposal and plan for your financial future.

- Consider Mediation: For couples who are able to communicate, mediation can be a constructive and cost-effective way to resolve financial issues. A neutral mediator can help you both understand the tax implications and work toward a mutually acceptable agreement, as encouraged by Connecticut's mediation programs (C.G.S. § 46b-53a).

Conclusion: Your Financial Future Matters

To summarize the key point: for any Connecticut divorce finalized after December 31, 2018, alimony is not taxable to the person who receives it and cannot be deducted by the person who pays it.

This fundamental change has reshaped divorce negotiations, placing a greater emphasis on the true, after-tax value of every dollar exchanged. While this may seem like just one more thing to worry about during an already difficult time, understanding the rules is the first step toward taking control of your financial future. By seeking knowledgeable legal and financial guidance, you can navigate this complexity and build a fair settlement that provides a stable foundation for your new beginning.

Legal Citations

- • C.G.S. § 25-30 View Source

- • C.G.S. § 46b-53a (Mediation Program) View Source

- • C.G.S. § 46b-66 (Review of Final Agreement) View Source

- • C.G.S. § 46b-81 (Assignment of Property) View Source

- • C.G.S. § 46b-82 (Alimony) View Source

- • C.G.S. § 46b-84 (Parents' Obligation for Child Support) View Source