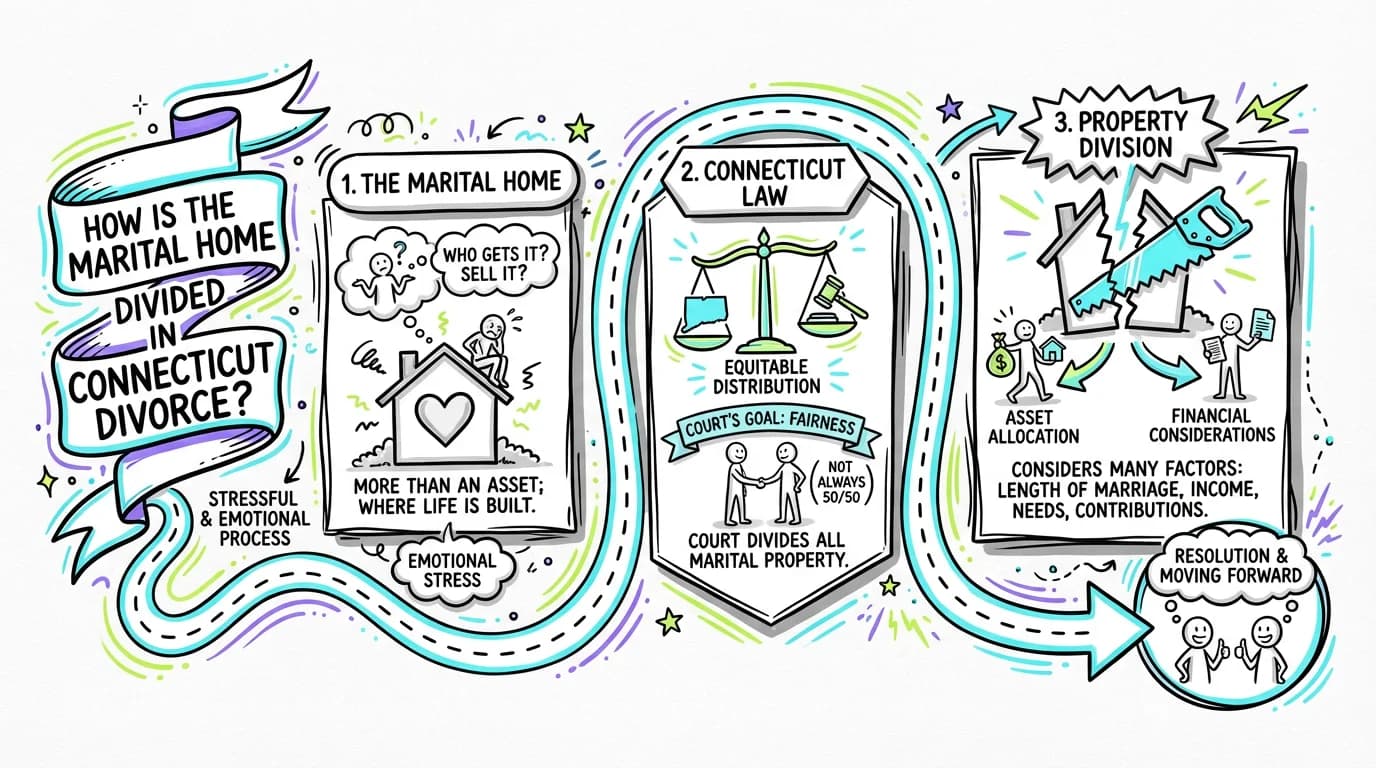

How is the marital home divided in Connecticut divorce?

Figuring out what happens to the family home is often one of the most stressful and emotional parts of a divorce. It’s more than just a financial asse...

Need help with your divorce? We can help you untangle everything.

Get Started Today

Figuring out what happens to the family home is often one of the most stressful and emotional parts of a divorce. It’s more than just a financial asset; it’s where you’ve built a life and raised a family. If you’re facing a marital home divorce in Connecticut, you’re likely wondering: Who gets the house? Do we have to sell it? How is it all decided?

The short answer is that Connecticut is an “equitable distribution” state. This means the court’s goal is to divide all marital property, including the home, in a way that is fair, which doesn’t always mean a 50/50 split. The decision isn't based on whose name is on the deed but on a wide range of factors specific to your family’s circumstances.

This guide will walk you through how Connecticut law handles the division of the marital home, the options available to you and your spouse, and the key factors a judge will consider to help you understand the process and make informed decisions during this challenging time.

Understanding Equitable Distribution and the Marital Home

In some states, marital property is divided equally. Connecticut takes a different approach. Under Connecticut law, the court has the authority to "assign to either spouse all or any part of the estate of the other spouse" (C.G.S. § 46b-81(a)). This principle is known as equitable distribution.

What does this mean for your house?

- All Property is on the Table: Connecticut is an "all-property" state. This means that everything owned by either you or your spouse is considered part of the marital estate and is subject to division. This includes the marital home, regardless of whether it was purchased before or during the marriage, or whether it was a gift or inheritance to one spouse.

- "Equitable" Means Fair, Not Equal: The court’s job is to arrive at a division that is fair and just under all the circumstances. This could be a 50/50 split, but it could also be 60/40, 70/30, or even 100/0 in some rare cases. The final division depends on how the judge weighs a specific set of legal factors.

- Title Doesn't Matter: It makes no difference whose name is on the deed or the mortgage. If the property was acquired by either spouse during the marriage, it is considered marital property. Even if one spouse owned the home before the marriage, the appreciation in its value during the marriage, and the home itself, are subject to division.

The court has broad discretion in deciding how to handle the marital home in a Connecticut divorce, aiming for a resolution that is fair to both parties based on their unique situation.

Connecticut Law: The Factors a Judge Considers

When deciding how to divide property, including the marital home, a Connecticut judge must consider a list of factors outlined in the law. According to Connecticut General Statutes § 46b-81(c), the court must consider:

- The length of the marriage: A long-term marriage might lead to a more equal division of assets than a very short one.

- The causes for the dissolution: While Connecticut is a no-fault state (meaning you can get divorced simply because the marriage has "broken down irretrievably"), the court can still consider fault, such as adultery or abuse, when dividing property.

- The age, health, station, and occupation of each party: The court looks at the overall condition of each spouse. For example, a spouse with significant health issues may have greater needs.

- The amount and sources of income, earning capacity, and employability: The court assesses each spouse's ability to support themselves financially after the divorce. A spouse with a much lower earning capacity might receive a larger share of the assets to ensure their future stability.

- The estate, liabilities, and needs of each party: This involves a full financial picture, including all assets (bank accounts, retirement funds, etc.) and all debts (mortgages, credit cards, loans).

- The opportunity for future acquisition of capital assets and income: The court considers each spouse's potential to earn and acquire assets in the future.

- The contribution of each of the parties in the acquisition, preservation or appreciation in value of their respective estates: This includes both financial contributions (like paying the mortgage) and non-financial contributions (like being a homemaker, raising children, or managing the household). The court recognizes that both types of contributions add value to the marital estate.

A judge is not required to give equal weight to each factor. They will look at the total picture and use their discretion to craft a property division order that they believe is equitable.

Common Options for Dividing the Marital Home

When it comes to the marital home in a Connecticut divorce, you and your spouse generally have three main options. If you can reach an agreement, the court will typically approve it as long as it's fair. If you can't agree, the court will decide for you.

1. Sell the House and Divide the Proceeds

This is often the cleanest and most common solution.

- How it works: You and your spouse agree to put the house on the market. Once it sells, you use the proceeds to pay off the mortgage, any home equity loans, real estate commissions, and other closing costs. The remaining profit (the equity) is then divided between you according to your settlement agreement or the court's order.

- Pros: It provides a clean financial break, allowing both spouses to move on with cash in hand to start their new lives. It also avoids future conflicts over the property.

- Cons: Selling a home can be emotionally difficult, especially if children are involved. Market conditions might not be ideal, and you'll have to pay transaction costs.

2. One Spouse Buys Out the Other

If one spouse wants to keep the house, a buyout is a popular option.

- How it works: First, you need to determine the home's fair market value, usually by getting a professional appraisal. Then, you calculate the home's equity (value minus mortgage and other liens). The spouse keeping the house pays the other spouse their share of the equity. This is typically done by refinancing the mortgage into their sole name or by trading other marital assets (like a retirement account) of equivalent value.

- Pros: Allows one spouse and the children to remain in the home, providing stability. The selling spouse still receives their share of the equity.

- Cons: The spouse keeping the house must be able to qualify for a new mortgage on their own, which can be difficult on a single income. It can also create a cash-flow problem if a large buyout payment is required.

3. Continue to Co-Own the House (Deferred Sale)

Though less common, some couples choose to continue owning the home together for a set period after the divorce.

- How it works: This is most often done to provide stability for minor children, allowing them to stay in the family home until a specific triggering event, such as the youngest child graduating from high school. The divorce agreement must be extremely detailed, specifying who pays the mortgage, taxes, insurance, and repairs, and what happens when the house is eventually sold.

- Pros: Provides continuity for children during a difficult transition. It may also allow you to wait for better market conditions before selling.

- Cons: It requires a high degree of cooperation and keeps you financially entangled with your ex-spouse, which can lead to future disputes.

If you cannot agree on one of these options, the court has the power to order a solution. Under C.G.S. § 46b-81(a), a judge can "order the sale of such real property" if they believe it's the proper way to carry out the divorce decree.

Important Considerations and Practical Advice

As you navigate the division of your marital home, keep these practical and legal points in mind:

- Automatic Orders: The moment a divorce is filed in Connecticut, automatic orders go into effect for both parties (Practice Book § 25-5). These orders prevent either spouse from selling, transferring, mortgaging, or otherwise disposing of any assets, including the marital home, without the other party's consent or a court order. This protects the marital estate from being depleted while the divorce is pending.

- Protecting Your Interest with a Lis Pendens: If you are concerned that your spouse might try to sell or mortgage the property without your knowledge (especially if your name is not on the deed), your attorney can file a lis pendens on the town land records. This is a formal notice that the property is the subject of a legal action. As stated in C.G.S. § 46b-80, this notice effectively prevents any sale or new mortgage on the property until the divorce is finalized, securing your financial interests.

- Getting a Professional Appraisal: Whether you plan to sell or do a buyout, getting an independent appraisal from a licensed real estate appraiser is crucial. This provides an objective, defensible valuation of the home, which is essential for fair negotiations and settlement.

- Capital Gains Tax: Be aware that selling the marital home could have tax implications. Consult with a financial advisor or tax professional to understand how capital gains taxes might affect you. There are often exemptions available for the sale of a primary residence, but it's important to plan ahead.

Frequently Asked Questions (FAQ)

Who gets to live in the house during the divorce?

If you and your spouse can't agree on who stays in the home while the divorce is pending, one party can file a motion for exclusive possession. The court can award temporary use of the family home to one spouse "as is just and equitable" (C.G.S. § 46b-83). The judge will consider factors like the children's best interests, the financial situation of each spouse, and any history of domestic violence.

Does it matter whose name is on the deed or mortgage?

No. In Connecticut, all property is subject to equitable distribution, regardless of title. The house is considered a marital asset even if only one spouse's name is on the deed.

What if the house was a gift or inheritance to one spouse?

Even if the house was a gift or inheritance to one spouse, it is still part of the marital estate and can be divided by the court. However, the source of the asset is one of the factors the judge will consider under C.G.S. § 46b-81(c). The court might decide it's more equitable to award that property (or a larger share of it) to the spouse who received it, but it is not required to do so.

Who pays the mortgage and bills for the house during the divorce?

This is determined by agreement or by temporary court orders. Often, the spouse with the higher income or the one remaining in the home will be ordered to pay the mortgage and utilities. These payments are typically tracked and may be credited back to the paying spouse in the final property settlement.

Can I force my spouse to sell the house?

If you and your spouse cannot agree on a buyout or another arrangement, you can ask the court to order the sale of the home. A judge has the authority under C.G.S. § 46b-81(a) to order the sale of real property to ensure a fair division of assets.

What happens if the house is "underwater" (worth less than the mortgage)?

If you owe more on your mortgage than the house is worth, this "negative equity" is treated as a marital debt. Like assets, marital debts must be divided equitably between the spouses. This could mean selling the house at a loss (a short sale) and splitting the remaining debt, or one spouse taking on the house and the associated debt as part of the overall settlement.

How does having children affect the division of the marital home?

The court's primary concern is the best interests of the children. While the law doesn't automatically grant the house to the custodial parent, the need to provide a stable home for the children is a significant factor. This may lead a judge to favor a buyout or a deferred sale arrangement that allows the children to remain in the home, at least for a period of time.

Getting Help

Deciding the fate of your marital home is a major financial and emotional decision. The complexities of Connecticut's equitable distribution laws make it essential to have experienced guidance.

- Consult a Connecticut Divorce Attorney: An experienced family law attorney can explain your rights, help you understand your options, and advocate for your best interests in negotiations or in court.

- Consider Mediation: If you and your spouse are able to communicate, mediation can be a less adversarial and more cost-effective way to reach an agreement about the house and other divorce-related issues. A neutral mediator helps facilitate your discussion and find common ground (C.G.S. § 46b-53a).

- Work with Financial Professionals: A financial advisor can help you understand the long-term financial impact of keeping or selling the home, while a mortgage broker can tell you if refinancing is a realistic option.

Conclusion

The question of how the marital home is divided in a Connecticut divorce doesn't have a one-size-fits-all answer. The process is guided by the principle of equitable distribution, where a judge considers numerous factors to reach a fair outcome. Whether you choose to sell the house, arrange a buyout, or pursue another path, the best solution is one that aligns with your family's unique financial and personal circumstances. By understanding the law and your options, you can approach this difficult decision with greater confidence and work toward a resolution that allows you to move forward.

Legal Citations

- • C.G.S. § 25-5 View Source

- • C.G.S. § 46b-53a (Mediation Program) View Source

- • C.G.S. § 46b-80 View Source

- • C.G.S. § 46b-81 (Assignment of Property) View Source

- • C.G.S. § 46b-83 (Alimony and Support Pendente Lite) View Source