How are debts divided in Connecticut divorce?

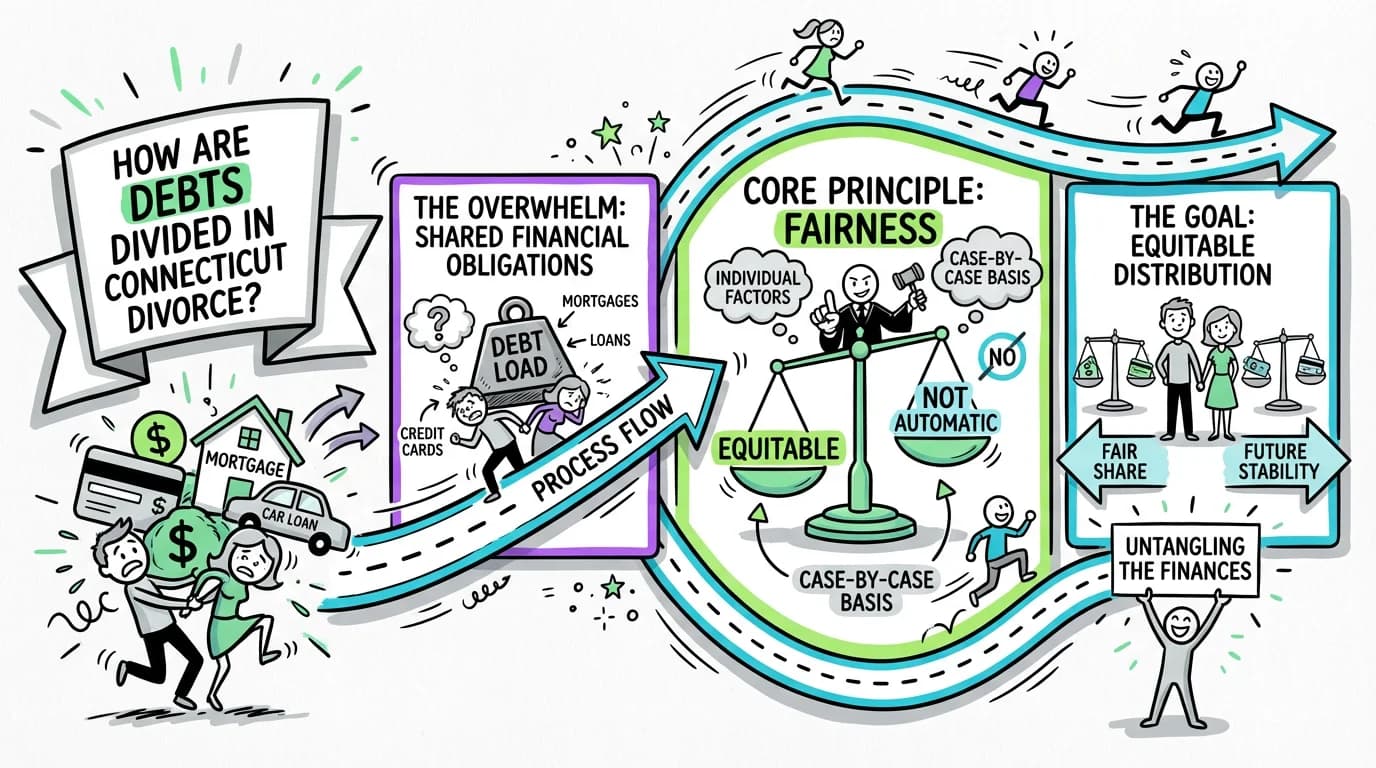

Figuring out what happens to your money and property during a divorce is stressful enough. But what about the other side of the coin—your debts? For m...

Need help with your divorce? We can help you untangle everything.

Get Started Today

Figuring out what happens to your money and property during a divorce is stressful enough. But what about the other side of the coin—your debts? For many couples, untangling shared financial obligations like mortgages, car loans, and credit card balances can feel even more overwhelming than dividing assets. If you’re wondering how debts are divided in a Connecticut divorce, you’re not alone, and the answer is rooted in a core principle of state law: fairness.

In Connecticut, there is no automatic 50/50 split. Instead, both assets and liabilities are divided based on a concept called equitable distribution. This means the court aims for a division that is fair and just under your specific circumstances, not necessarily an equal one. The court has broad discretion to decide who pays what, regardless of whose name is on the account.

This guide will walk you through exactly how Connecticut courts approach the division of debt, the laws that govern the process, and the practical steps you can take to protect your financial future.

Understanding Equitable Distribution and Debt

Before we dive into the details, it’s essential to understand the legal foundation for how all property, including debt, is handled in a Connecticut divorce. The state operates under an "all-property" equitable distribution model.

This means that virtually everything owned by either spouse—and every debt owed by either spouse—is considered part of the marital estate and is on the table for division. It doesn't matter if the debt was acquired before the marriage or if it's only in one person's name. The court has the authority to assign responsibility for any liability to either party.

The key question the court asks is not "Whose debt is this?" but rather "What is the most equitable way to assign this debt?" The final allocation of how debts are divided in a Connecticut divorce will depend on a long list of factors that paint a complete picture of your marriage and financial situation.

Connecticut Law: The Factors That Matter

The rules for dividing property and debt are outlined in the Connecticut General Statutes. The most important statute is C.G.S. § 46b-81(c), which lists the specific factors a judge must consider. While this law speaks about assigning "the estate" of the parties, it applies equally to liabilities.

According to C.G.S. § 46b-81(c), when determining how property and debts will be divided, the court must consider:

- The length of the marriage: In shorter marriages, the court may be more likely to return each party to their pre-marital financial position. In longer marriages, finances are seen as more intertwined.

- The causes for the divorce: If one spouse’s behavior led to the breakdown of the marriage (e.g., through financial misconduct like gambling or spending marital assets on an affair), the court can consider that. This could mean assigning the debt incurred from that behavior to the responsible spouse.

- The age and health of each spouse: A spouse with significant health issues or who is older may have a greater need for financial support and may be assigned less debt.

- Station, occupation, and sources of income: The court looks at each person's lifestyle, job, and how they earn money.

- Earning capacity, vocational skills, education, and employability: A spouse with a high-paying job or the ability to earn significantly more in the future may be ordered to take on a larger portion of the marital debt.

- The estate, liabilities, and needs of each party: This is a direct look at the complete financial picture—what you own, what you owe, and what you each need to move forward.

- The opportunity for future acquisition of capital assets and income: Similar to earning capacity, this factor considers each spouse's potential to build wealth in the future.

- The contribution of each spouse to the acquisition, preservation, or appreciation in value of the estate: This includes non-monetary contributions, like a stay-at-home parent’s work in managing the household and raising children, which allowed the other spouse to advance their career.

The court weighs all these factors together to arrive at a final decision on how debts are divided in a Connecticut divorce. There is no magic formula; the outcome is tailored to the unique facts of each case.

The Step-by-Step Process for Handling Debt

Navigating the division of debt can feel chaotic. Following a structured process can help you gain clarity and control.

Step 1: Identify and List Every Single Debt

You can't divide what you don't know about. The first step is to create a complete inventory of all outstanding liabilities. This includes:

- Mortgage loans and home equity lines of credit (HELOCs)

- Car loans

- Credit card balances (for both joint and individual cards)

- Student loans

- Medical and dental bills

- Personal loans from banks or family members

- Tax debt (federal and state)

- Business loans

It's a good idea for both you and your spouse to pull your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) to ensure nothing is missed.

Step 2: Complete Your Financial Statement

In every Connecticut divorce, both parties are required to file a sworn financial statement with the court (Practice Book § 25-30). This official form (JD-FM-6) is where you must list all your income, expenses, assets, and—most importantly for this topic—your liabilities.

This is arguably the most important document you will file in your divorce. Be thorough, accurate, and honest. Hiding debts or assets can have serious consequences. You must list all debts, whether they are in your name, your spouse's name, or held jointly.

Step 3: Gather Your Documentation

For each debt, gather as much paperwork as you can, including:

- Recent statements showing the current balance.

- The original loan agreement or credit card agreement.

- Proof of what the debt was used for (e.g., statements showing charges for home repairs versus personal luxury items).

This documentation helps the court understand the nature of each debt, which can influence how it's assigned.

Step 4: Negotiate a Settlement Agreement

The vast majority of divorces in Connecticut are settled by agreement rather than by a judge after a trial. You and your spouse, often with the help of attorneys or a mediator, will negotiate how to handle each liability.

For example, you might agree that the person keeping the house will be responsible for the mortgage, or that you will split a credit card balance based on who made the charges. This agreement, once finalized, is submitted to the court.

Step 5: The Court's Final Order

If you reach an agreement, a judge will review it to ensure it is "fair and equitable under all the circumstances" (C.G.S. § 46b-66). If the judge approves it, your agreement becomes a legally binding court order.

If you cannot agree, you will proceed to a trial. After hearing evidence from both sides, the judge will issue a final order detailing exactly how the debts are divided, based on the C.G.S. § 46b-81 factors.

Important Considerations and Practical Advice

Getting a court order is one thing; protecting yourself financially is another. Here are some critical points to keep in mind.

Creditors Are Not Bound by Your Divorce Decree

This is a crucial and often misunderstood point. Your divorce decree is a contract between you and your ex-spouse that is enforceable by the family court. It is not binding on your creditors.

If your name is on a joint credit card, and the divorce decree says your ex-spouse is responsible for paying it, the credit card company can still come after you if your ex fails to pay. From the creditor's perspective, you are both still 100% responsible for the entire balance until it's paid in full.

How to Protect Yourself Post-Divorce

Because creditors aren't bound by your decree, you need to take proactive steps to separate your financial lives.

- Close Joint Accounts: As soon as possible, close all joint credit card accounts and open new ones in your individual names.

- Refinance Joint Debts: For larger debts like mortgages and car loans, the best solution is to have the person responsible for the debt refinance it solely in their name. This officially removes your name and liability.

- Include an Indemnification Clause: Your settlement agreement should include an "indemnification" or "hold harmless" clause. This language states that if your ex-spouse fails to pay a debt assigned to them and the creditor comes after you, you can take your ex back to family court to be reimbursed for what you had to pay, plus any legal fees you incurred.

Automatic Court Orders

When a divorce is filed in Connecticut, automatic court orders go into effect for both parties (Practice Book § 25-5). These orders prohibit you from, among other things, "incurring unreasonable debts," including borrowing against assets or running up credit cards, except for customary household expenses or reasonable attorney's fees. This prevents one spouse from intentionally creating debt to harm the other during the divorce process.

Frequently Asked Questions About Dividing Debt

Here are answers to some common questions about how debts are divided in a Connecticut divorce.

Q: What if my spouse ran up secret credit card debt in their name only? Am I responsible?

A: You might be. Because Connecticut is an "all-property" state, a debt in one spouse's name can still be considered a marital liability. The court will look at what the debt was for. If it was used for family expenses (groceries, kids' clothes, car repairs), it's more likely to be divided between you. If it was used for purposes that didn't benefit the marriage (like a secret vacation or gambling), the judge has the discretion to assign the entire debt to your spouse.

Q: Am I responsible for my spouse's student loans from before we were married?

A: It's possible, but less likely. Pre-marital debt is often, but not always, assigned to the person who incurred it. However, the court will consider whether the marital partnership benefited from the degree financed by the loans. If your spouse's education led to a higher-paying job that benefited the whole family, the court might assign a portion of that debt to you, especially in a long-term marriage.

Q: What happens if my ex is ordered to pay a joint debt but doesn't?

A: The creditor can and likely will pursue you for payment. Your recourse is to file a Motion for Contempt with the family court. If the judge finds your ex in contempt for violating the divorce decree, they can be ordered to pay, fined, or even incarcerated. The indemnification clause in your agreement is key here, as it allows you to ask the court to force your ex to repay you for any money you had to pay the creditor.

Q: Is it always a 50/50 split of debts in Connecticut?

A: No. This is a common misconception. Connecticut law requires an equitable split, which means fair, not necessarily equal. A 60/40, 70/30, or even 100/0 split is possible depending on the factors in C.G.S. § 46b-81.

Q: Should we try to pay off joint debt before filing for divorce?

A: If you have the means and can agree on how to do it, paying off joint debt can simplify the divorce process significantly. Using joint savings to clear a joint credit card balance, for example, removes one item from the negotiation table. However, you should not drain your personal savings to pay a joint debt without first consulting an attorney.

Q: How is the mortgage on our house handled?

A: The mortgage is tied to the house. Typically, the person who keeps the house is responsible for paying the mortgage. The ideal scenario is for that person to refinance the mortgage into their sole name, which removes the other spouse from the loan and pays them their share of the home's equity. If refinancing isn't possible, the parties may agree to sell the house and divide the proceeds (and pay off the mortgage).

Q: Can I be forced to pay my spouse's legal fees for the divorce?

A: Yes. Under C.G.S. § 46b-62, the court can order one party to pay the other's "reasonable attorney's fees" based on their respective financial abilities and the criteria for alimony. This is often done when there is a significant disparity in income or assets, ensuring both parties have access to legal representation.

Getting Help

The process of how debts are divided in a Connecticut divorce is complex and depends heavily on the specific facts of your case. While this article provides general information, it is not a substitute for legal advice.

Consulting with an experienced Connecticut divorce attorney is the best way to understand your rights and obligations. An attorney can help you create a full picture of your financial situation, negotiate a fair settlement, and ensure your final divorce decree includes the protections you need to move forward with financial security. For couples who are largely in agreement, divorce mediation (C.G.S. § 46b-53a) can also be an effective and less adversarial way to resolve these issues.

Conclusion

Dividing debt is a challenging but manageable part of the divorce process in Connecticut. The key is to remember that the goal is equity, not equality. By being thorough in your financial disclosures, understanding the factors the court considers, and taking proactive steps to separate your financial lives, you can navigate this process and lay the groundwork for a stable financial future. Remember to be organized, be honest, and seek professional guidance to protect your interests.

Legal Citations

- • C.G.S. § 25-30 View Source

- • C.G.S. § 25-5 View Source

- • C.G.S. § 46b-53a (Mediation Program) View Source

- • C.G.S. § 46b-62 (Attorney Fees) View Source

- • C.G.S. § 46b-66 (Review of Final Agreement) View Source

- • C.G.S. § 46b-81 (Assignment of Property) View Source